Business Email Compromise (BEC) has crossed a critical threshold for Indian organizations. What was once treated as a cyber fraud issue is now a material business risk with direct implications for revenue protection, audit outcomes, regulatory confidence, and executive accountability.

CFO fraud driven by BEC no longer exploits technical weaknesses alone. It exploits trust, authority, and speed- three pillars on which modern digital finance operates.

Indian enterprises are operating in high-velocity financial environments. Real-time payments, distributed approval models, and email-led workflows have dramatically improved efficiency. At the same time, they have collapsed decision buffers that

previously absorbed verification delays.

In this environment, a single compromised or impersonated email can trigger irreversible financial exposure within minutes. The shift from post-incident remediation to instant loss defines why BEC now belongs on board and audit committee agendas.

BEC in India has evolved from volume-driven phishing into intelligence-led financial manipulation. Attackers study organizational hierarchies, payment calendars, vendor relationships, and approval norms before acting.

Finance, treasury, and procurement teams have become primary targets- not because of weak security controls, but because email remains an implicit approval mechanism during critical payment windows.

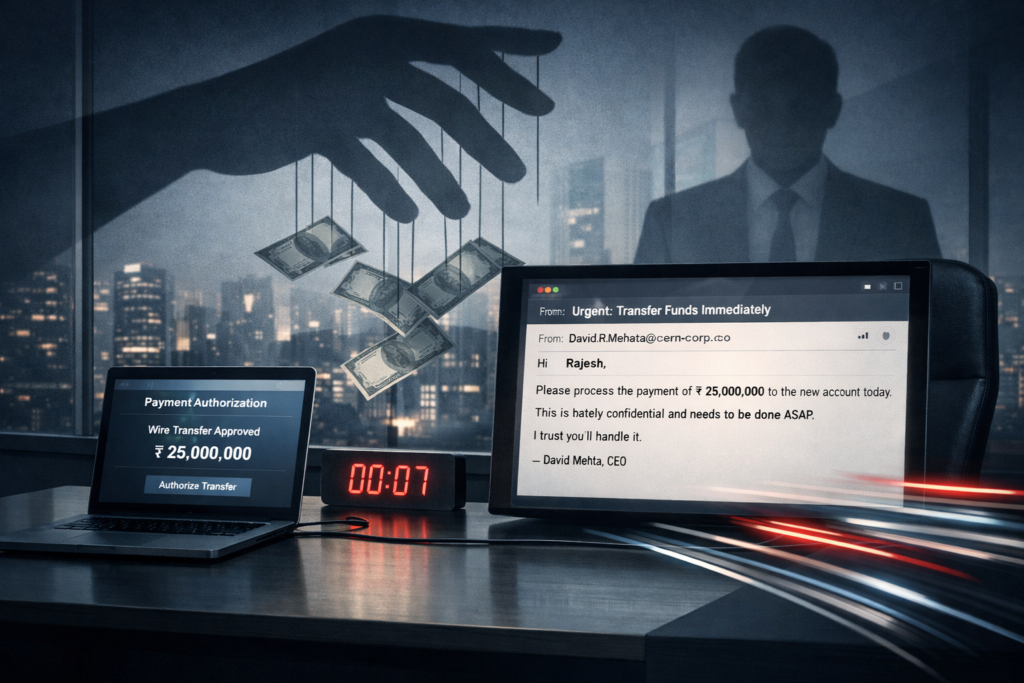

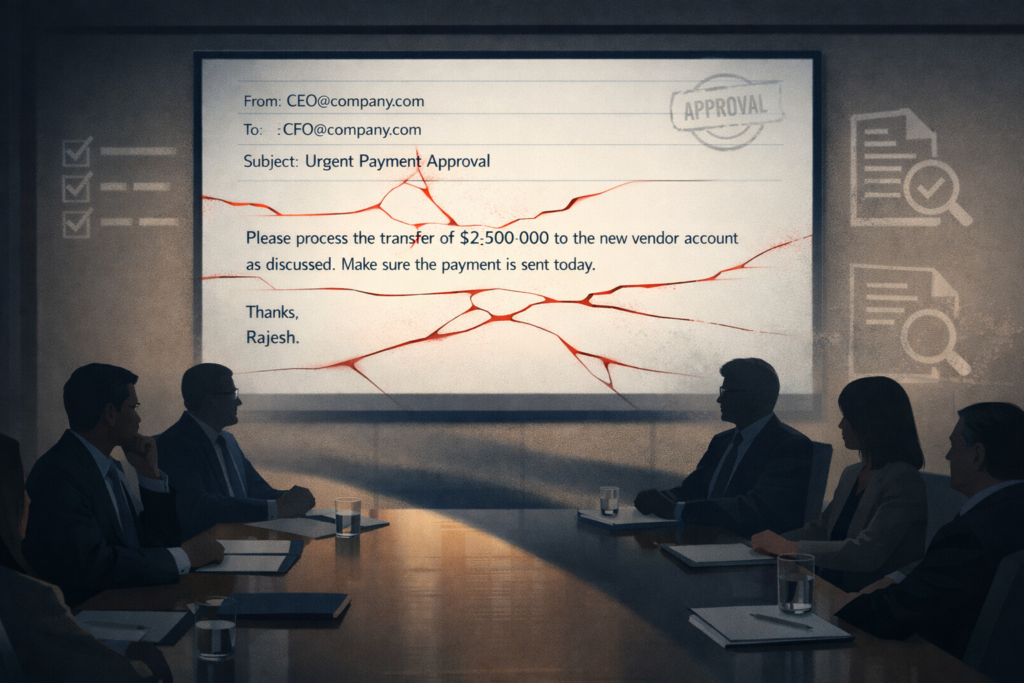

The most damaging BEC incidents manifest as CFO fraud. Attackers impersonate senior executives and issue urgent instructions that bypass established controls.

Authority-driven urgency suppresses verification, overrides segregation of duties, and exploits the natural bias toward operational continuity. In these cases, human trust-not infrastructure- becomes the primary attack surface.

Common BEC techniques include executive impersonation using lookalike domains, display-name spoofing, and replicated email signatures. Vendor account compromise is equally prevalent, with attackers inserting themselves into live billing cycles and redirecting payment instructions at precisely the right moment.

These attacks succeed because they blend seamlessly into legitimate business communication, avoiding traditional security alerts.

Several structural factors are driving growth. Real-time payments reduce verification tolerance. Email continues to be treated as sufficient authorization for high-value transactions. Critically, ownership of BEC risk often sits outside cybersecurity functions, despite finance teams bearing the losses.

As digital transformation accelerates faster than financial governance reform, exposure continues to expand across BFSI, manufacturing, IT services, healthcare, and export-driven sectors.

Financial recovery from BEC is rare. Funds typically move out of recoverable channels within hours. The longer-term damage, however, is often more severe.

CFO fraud incidents expose gaps in governance, control discipline, and executive oversight. Auditors and regulators increasingly evaluate decision accountability rather than technical failure. Investor and board trust erodes long after the

incident is closed.

Technology controls matters but they are not sufficient on their own. Strong identity assurance through email authentication standards, MFA, and mailbox protection reduces impersonation risk. More importantly, payment verification must be treated as a governance mandate. Independent confirmation channels and enforced segregation of duties must remain non-negotiable, even under time pressure.

When BEC occurs, outcomes depend on minutes-not days. Immediate bank coordination, credential isolation, and forensic preservation determine whether funds can be frozen and whether regulatory defensibility is preserved.

Prepared organizations rehearse these steps in advance. Unprepared ones learn under scrutiny.

BEC resilience is ultimately cultural. Executives must normalize verification and challenge, removing stigma from confirmation and delay.

Boards must treat CFO fraud as an enterprise financial risk with defined controls, testing cadence, and accountability metrics. Where leadership sets the tone, fraud success rates fall sharply.

Business Email Compromise represents a sustained financial and governance threat across Indian organizations. The most damaging incidents reveal not technology gaps, but leadership and process weaknesses. Enterprises that embed verification discipline, executive accountability, and resilient financial controls will be better positioned to withstand financial loss, regulatory scrutiny, and long-term trust erosion in India’s rapidly digitizing

economy.